(© JenkoAtaman - stock.adobe.com)

In a Nutshell

- A national survey of 1,421 U.S. adults found that, on average, just $6,356 of additional debt beyond existing obligations would be enough to push Americans into bankruptcy.

- The cost-of-living crisis (43.4%) and increased tariffs (41.7%) were by far the leading contributors to bankruptcy, outpacing personal financial missteps such as overspending or poor planning.

- Filing for bankruptcy ranked as more stressful than buying a first home, having a child, and experiencing bereavement, with divorce being the only life event considered comparably difficult.

Three months. That’s all the financial cushion most Americans say they have before the bills start going unpaid. Lose a job, face a medical emergency, or absorb one too many price hikes, and roughly four in ten adults would be out of options in about 90 days.

That figure comes from a national survey of 1,421 adults conducted in February 2026 by JG Wentworth, a financial services company specializing in debt relief. When asked how long they could cover basic living expenses if their income suddenly stopped, 40.8% of respondents said three months. Another 9.5% said two months, and 5.4% said less than one. On the other end, just 3% said they could stretch their savings beyond six months. For most households, the financial margin between stability and crisis is razor-thin.

What makes that number land harder is what lies on the other side of it. According to the same survey, it takes an average of just $6,356 in additional debt beyond existing obligations to push an American household toward bankruptcy. Non-business bankruptcy filings rose 10.8% between September 2024 and September 2025, per federal court data, and the survey’s findings go a long way toward explaining why: a growing share of Americans simply don’t have enough buffer to absorb a bad month, let alone a prolonged financial shock.

A Financial System Built on Fumes

When respondents who had filed for bankruptcy were asked what triggered it, the top answers weren’t personal missteps. The cost-of-living crisis led the way at 43.4%, followed closely by the impact of increased tariffs at 41.7%. Tariffs are taxes on imported goods — when companies pay more to bring products into the country, those costs tend to get passed along as higher prices at the register. Medical expenses ranked third at 3.7%, with credit card or personal loan debt (3.2%) and job loss (2.6%) rounding out the top five.

Overspending, poor financial planning, and mortgage or interest rate increases each registered at 0.3% or below. For most filers, bankruptcy wasn’t the result of living beyond their means. It was the result of the means themselves running dry.

Among participants who had never filed for bankruptcy, 45.5% said they are managing comfortably. Among those who had filed, only 5.6% said the same.

The main contributors to bankruptcy

| Rank | What was the main contributor that led to bankruptcy? | Percentage of participants |

|---|---|---|

| 1 | Cost of living crisis | 43.40% |

| 2 | Increased tariffs | 41.70% |

| 3 | Medical expenses | 3.70% |

| 4 | Credit card or personal loan debt | 3.20% |

| 5 | Job loss or reduced income | 2.60% |

| 6 | Business failure | 1.60% |

| 7 | Student loans | 1.10% |

| 8 | Overspending / lifestyle choices | 0.70% |

| 9 | Divorce or family breakdown | 0.50% |

| 10T | Interest rate increases | 0.30% |

| 10T | Mortgage increases | 0.30% |

| 10T | Poor financial planning | 0.30% |

| 13T | Death of a loved one (i.e. funeral costs) | 0.20% |

| 13T | Other unexpected expenses | 0.20% |

When There’s No Cushion, Essentials Are the First to Go

Nearly nine in ten respondents (86.9%) said they had already skipped an essential payment at some point due to financial pressure. Rent was the most commonly missed obligation (60.4%), followed by mortgage payments (59.9%) and gasoline (48.9%). Medical insurance (38.2%) and doctor visits (26.2%) also made the list.

When asked what they would cut first if things got worse, dining out topped the list (72.2%), followed by takeout orders (70.3%) and coffee (58.6%). Streaming services and concert tickets followed. What participants were least willing to give up: socializing (7.2%), attending events like weddings and birthdays (7.2%), and buying gifts for others (8%). Even under financial duress, social connection appears to function as its own kind of necessity.

As for actual crisis response, the first move most said they’d make was cutting expenses (41.5%), followed by declaring bankruptcy (34.6%). Borrowing from family or friends ranked last as a first step (5.3%), even though 79.4% said they’d eventually consider it. The gap between what people would do first and what they’d ultimately resort to tells its own story about how quickly options narrow once income disappears.

Bankruptcy’s Lasting Damage Goes Beyond the Credit Score

Recovery from bankruptcy is possible, but it doesn’t arrive quickly or cleanly. Among those who had filed, 89.3% said they eventually rebuilt their finances, with most taking three to five years. Just 1% said they were still struggling as a direct result of the filing.

But “financially recovered” and “unaffected” are not the same thing. An overwhelming 97.8% of filers said they are still feeling the effects of their bankruptcy today, regardless of how long ago they filed. Nearly three quarters (73.7%) reported ongoing difficulty obtaining loans or credit, and 73.3% said their credit score remains damaged. For 71.2%, bankruptcy had at some point prevented them from renting a home or apartment. Another 70.5% said it blocked them from buying property, and 60.7% said it stood between them and a loan or mortgage.

Among those who hadn’t fully recovered financially, the main barriers were high living costs (88.4%), low income or unemployment (85.8%), and continued medical expenses (82.5%). Lack of financial knowledge or guidance ranked far lower, at 4.2%, again pointing away from personal behavior and toward structural conditions as the primary obstacle.

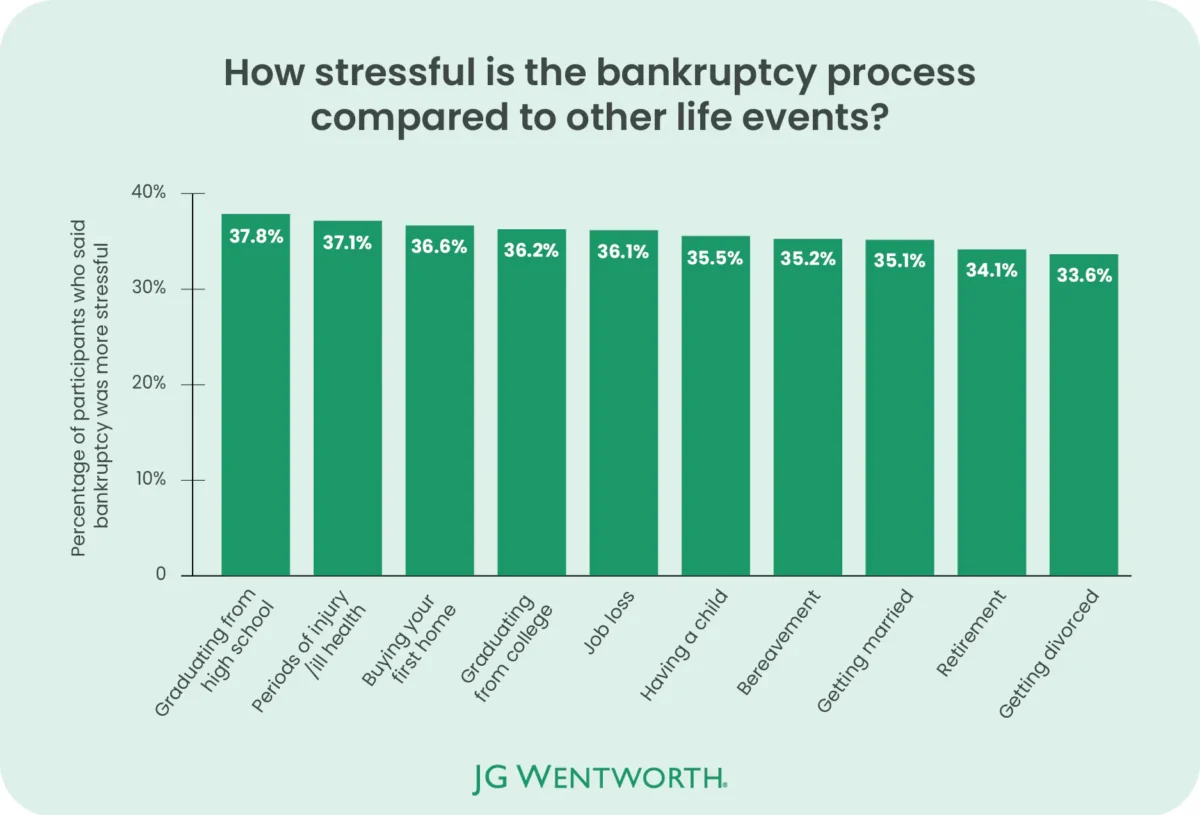

The experience also carries an emotional toll that rivals some of life’s most demanding events. Among those who had filed, more than a third said bankruptcy was more stressful than buying their first home (36.6%) or having a child (35.5%). Divorce was the only comparable benchmark, landing at roughly the same stress level as the bankruptcy process itself.

When asked what would most improve their financial security going forward, the top answer across all respondents was increasing income or job stability (33.4%), followed by better financial education or guidance (27.4%) and broader health insurance coverage (22.3%). For most, the prescription is straightforward. The harder question is whether the conditions that allow it are actually within reach.

About the Survey

JG Wentworth, a financial services company specializing in structured settlements, annuity purchasing, and debt relief, conducted this survey in February 2026. A total of 1,421 adults across the United States participated, drawn from a range of backgrounds. The survey covered topics including what contributes to bankruptcy, the emotional stress of the filing process, coping strategies, and how bankruptcy affects spending habits and long-term financial stability. For questions where multiple answers were permitted, totals may exceed 100%.

Demographics

Respondents were 57.7% female, 41.9% male, 0.1% non-binary, and 0.3% preferred not to say. By age, the largest group fell between 29 and 44 years old (69.7%), followed by 18 to 28 (21.5%), 45 to 60 (7.2%), 61 to 79 (1.5%), and 80 and older (0.1%).

Limitations

Because the survey was commissioned and published by JG Wentworth, a company with a financial interest in topics related to debt and bankruptcy, the results should be interpreted with that context in mind. The sample skewed heavily toward adults aged 29 to 44, which may not fully represent the experiences of older Americans or younger adults just entering the workforce. The survey relied on self-reported data, meaning responses reflect participants’ perceptions and recollections rather than verified financial records. Additionally, participants who had filed for bankruptcy were not screened for chapter type (Chapter 7 versus Chapter 13, for example), which carry meaningfully different terms and timelines, and that distinction could affect how respondents answered questions about recovery and lasting effects.

Self reporting is an extremely poor method of collection. How many people are going to own up to poor financial planning or lifestyle choices? Very few indeed.

Really? You need a study to tell you people are a couple missed paychecks from ruin? Most of the planet lives with zero savings.

NEW RULE: No one graduates HS without 2 semesters of financial literacy. Hit them again in college.

Who cares?

Are we great again yet?

No, but Trump and his family are supposedly $5 Billion wealthier than when he won the election,, not to mention not have several indictments go to trial that would have proved his guilt.

AS a Lender I am on the other side of the equation, a side never given a voice. Having executed several bankruptcy recently I can comment that most Bankrupts are liars and cheats. They have not paid in months, sometimes a year or more. They use every method to weasel their way out with the full and FREE help from every possible Government agency.

Meanwhile I am losing thousands every month in payments and late fees, not to mention tens of thousand in Attorney’s fees.

When a bankruptcy is finally resolved the the Bankrupt has six months to buy the property back.

So, as a lender I’m without income on my investment for at least a year and more likely two or more years.

So, how about doing a “Study Finds” on the other side of the story? (Didn’t think so.)