(Photo by Feng Yu on Shutterstock)

In A Nutshell

- Americans now perceive inflation to be far higher than it really is, with a sharp divergence since Donald Trump’s second term began.

- In May 2025, people expected prices to rise by 6.6%, but official inflation was just 2.4%.

- Rising food and housing costs partly explain the gap, but political uncertainty, tariffs, and a weaker dollar are fueling public fears.

- Trump’s economic policies, including attempts to shake up the Federal Reserve and a $4.5 trillion tax cut, have heightened expectations of future inflation.

- Inflation perceptions directly shape consumer spending and also track closely with Trump’s sinking job approval ratings.

American voters often rank inflation as the most important issue facing the U.S. But something odd has happened to inflationary expectations since Donald Trump became president in January. Americans believe inflation is much higher than it is, and are bracing themselves for further increases.

The difference between real inflation and what the public think it is has diverged by a significant amount – much more so than under former president Joe Biden.

In December 2024, while Biden was still in office, respondents in surveys conducted by the University of Michigan predicted a rate of inflation of 2.8%, when it was actually 2.7%. However, by May 2025, five months into Trump’s second term, the public was estimating inflation at 6.6% when inflation had fallen to 2.4%.

The inflation expectations surveys included the following question: “By about what percent do you expect prices to go up/down on the average, during the next 12 months?”

The chart below shows the average response to this question over four years. This tells us what the average American feels about price increases, rather than what is actually happening in the economy. These views directly affect spending by consumers and therefore growth and employment in the U.S. economy.

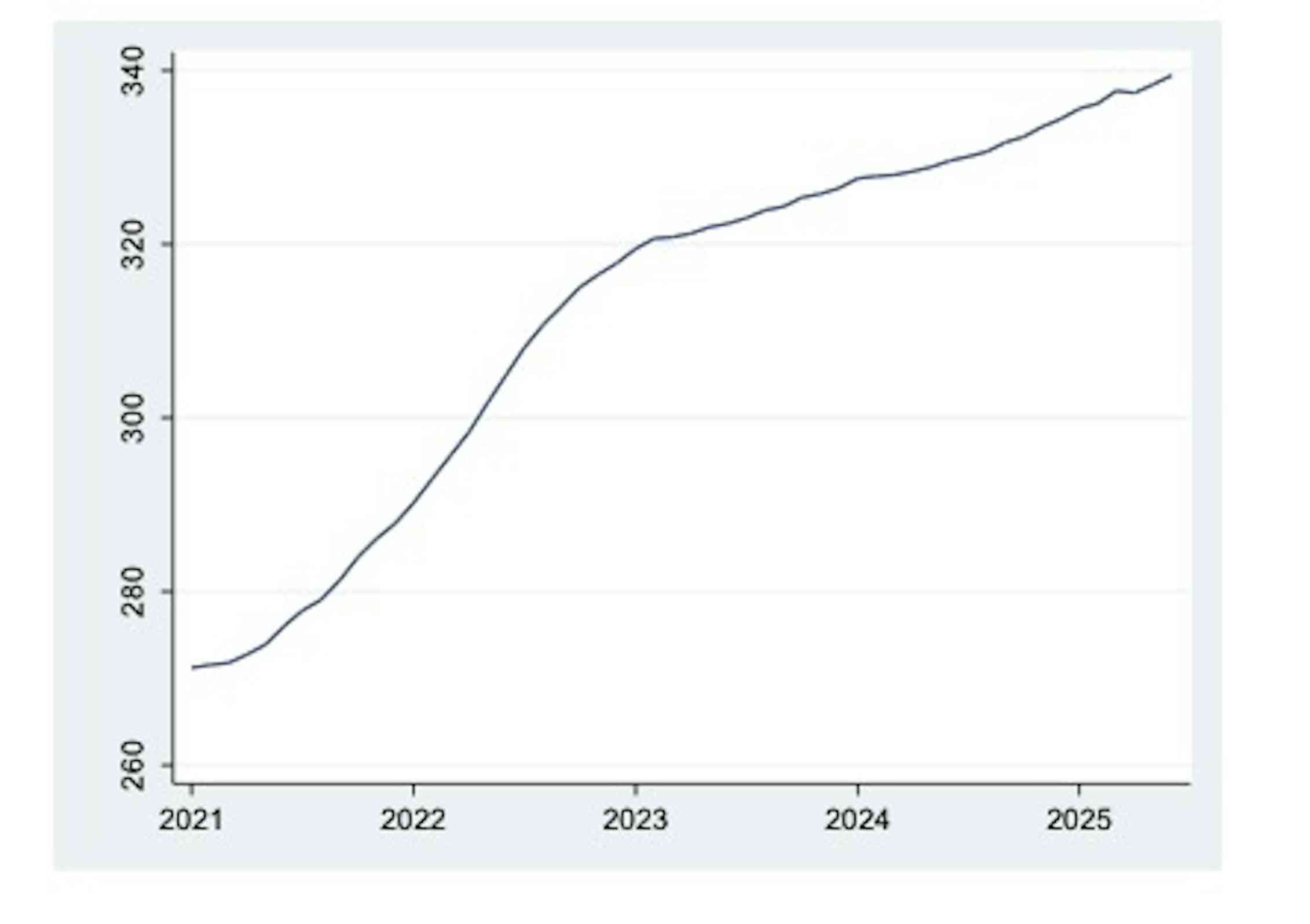

Expectations and actual inflation 2021 to 2025:

The red line on the chart above shows the actual inflation rate in the U.S., measured by the annual change in the consumer price index. It starts from former U.S. president Joe Biden’s inauguration as president in January 2021 when the pandemic had a big impact on inflation. Subsequently, the rate has been declining since early 2022 although there was a modest increase from the start of Donald Trump’s second term from January 25 this year.

Some of these expectations can be explained by specific items. For example, food prices in the U.S. have continued to increase as the chart below shows. The increases were rather rapid after the end of the pandemic, and they have continued but at a slower rate from the start of 2023, even though the broader inflation rate was falling at the time. Food prices are a particularly sensitive item because food is an essential.

Another item is the rapid rise in house prices that started after the pandemic and has continued under the Trump administration. This has put home ownership beyond the means of many Americans. However, neither of these can fully explain why the public believe inflation is so much higher than it actually is since the start of Trump’s second term in office.

Consumer food price index in the US 2021 to 2025:

A reason for this concern among the U.S. public could be the financial uncertainty among businesses and financial markets and consumers.

Donald Trump’s attempts to sack Lisa Cook, the governor of the Federal Reserve, currently held up by the courts, is one example of a factor creating economic instability. The Fed is an independent institution that controls inflation via changes in interest rates and so dramatic changes there are likely to create worries about what happens next.

What About Tariffs?

The introduction of high tariffs on goods from other countries by the Trump administration is probably another factor. Put simply, tariffs are a tax on imports and so have a direct impact on the price of goods on sale in the U.S.

This, coupled with a fall in the value of the dollar in recent months, will be pushing up prices in American shops. A dollar would buy 98 euro cents in January of this year, almost a one-for-one exchange rate. By August 25, it would buy only 85 euro cents, a fall in value of around 15%.

Trump’s so-called “big beautiful bill,” which passed Congress in July, could be another source of inflationary expectations. This extends the tax cuts introduced in Trump’s first term, reducing taxes by U.S. $4.5 trillion over ten years while cutting welfare spending and reducing investments in green energy projects.

The Yale University Budget Lab, a research center studying financial policy, estimates that the bill will add $3 trillion to the nation’s debt over the period 2025-2034 and $12.1 trillion from 2025-55. This means that the U.S. Treasury has to pay higher rates to encourage lenders when they become nervous about the inflationary consequences of the deficits.

If a country has to borrow large amounts to balance the books, it creates a temptation to print more money, which then boosts inflation.

When it comes to the political consequences of this, inflationary expectations are really important. This is because the public’s judgment about the president’s handling of inflation are largely the same as judgments about his overall presidency.

This can be seen in the chart below, which comes from successive surveys conducted by YouGov for the Economist newspaper since Trump came to office.

Approval ratings for the president’s handling of inflation and his overall job ratings:

The chart compares Trump’s overall job approval with his approval ratings for handling inflation. They track very closely – and both are rapidly falling, indicating that the failure to combat inflation is tarnishing the president’s approval ratings.

Presidential job approval is closely related to voting behavior, so if inflation continues to rise and the public believe it will be even higher in the future, then this is likely to damage both Trump and the Republican party in the midterm elections next year.

Paul Whiteley, Professor, Department of Government, University of Essex. He has received funding from the British Academy and the ESRC.

This article is republished from The Conversation under a Creative Commons license. Read the original article.

![]()